What Is a Credit Score?

A credit score is a three-digit number used by lenders to assess your creditworthiness. Credit scores let lenders and creditors know how much of a risk you pose as a borrower, indicating your ability to pay your bills on time. This number guides their lending decisions on credit limits, loan terms and interest rates.

How Do Credit Scores Work?

Credit scoring models analyze credit reports from the three major credit monitoring agencies and assign a score to the consumer based on that data.

There are different credit scoring systems available, and each lender will favor one over the other. Some are for general use, while others are tailored to specific lending industries like mortgage and auto loans.

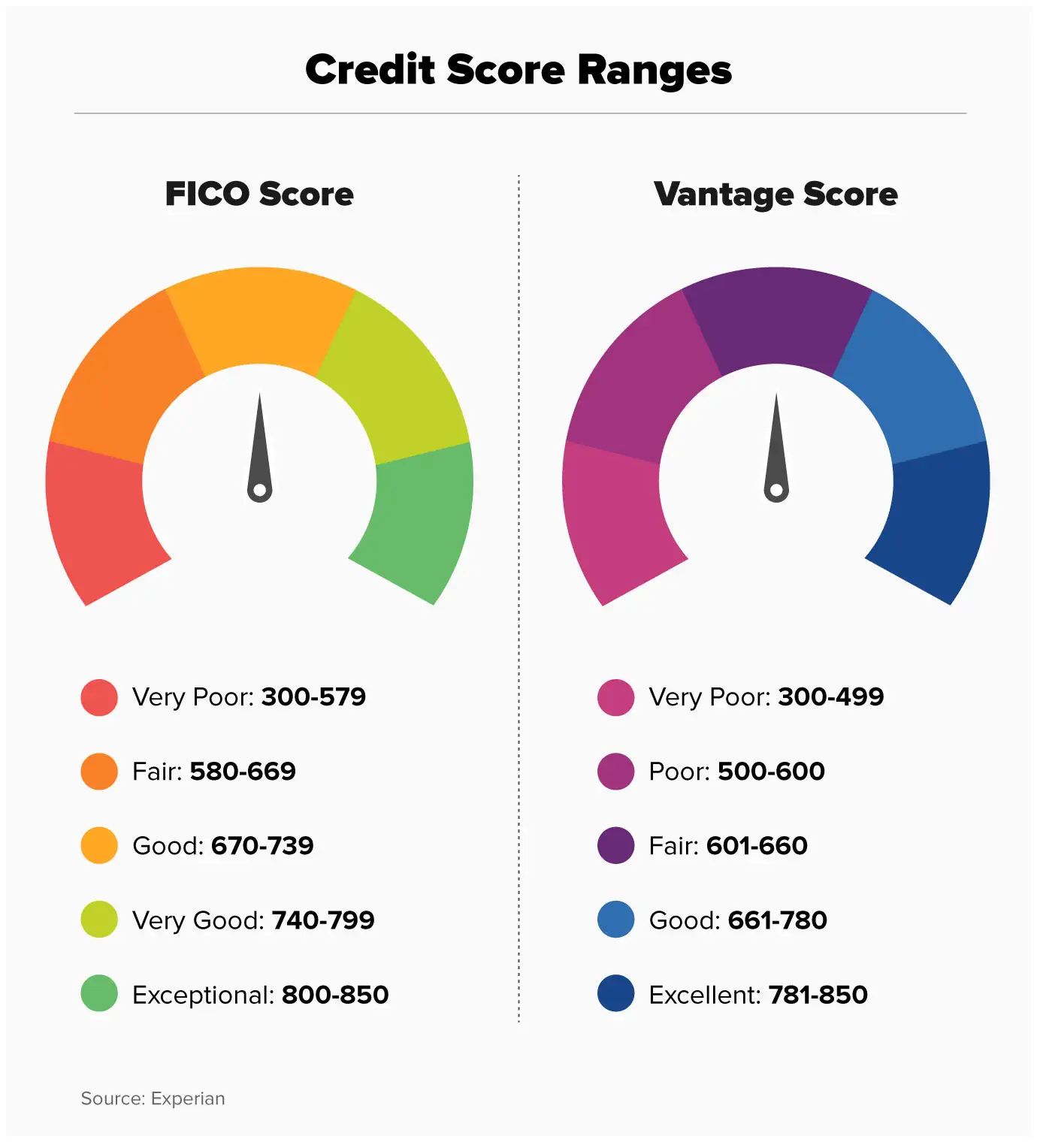

The most widely used are FICO (Fair Isaac Corporation) and VantageScore 3.0.

Both FICOand VantageScore provide free credit scores and tools that help identify bad credit and create personal finance plans.

How are credit scores calculated?

Every score is based on information gathered by the major credit bureaus: Experian, Equifax, and TransUnion. These credit reporting agencies gather data from credit card companies, financial institutions, and lenders to create a report.

Credit scoring models analyze the credit report information and assign value to each factor. Depending on the model, some factors will be highly influential while others only account for a small percentage of your overall score. As a result, different scoring models will produce different credit scores, even if they reference the same credit report.

Difference between credit scores and credit reports

Your credit score is not the same as your credit report. Credit scoring companies use the information on your credit report to determine your credit score.

A credit report documents your credit and payment history. It’s the information contained within your credit report that determines your creditworthiness and, consequently, your score. Anyone can obtain their free credit report from Annual Credit Report (annualcreditreport.com) or directly from one of the credit bureaus.

It’s important to regularly check your own credit report to spot items that could inflict long-term damage on your credit. Lenders look at one of three credit reports, so make sure the information is correct and that it matches across agencies.

Factors That Make Up Your Credit Score

- Payment history: Paying on time improves credit scores, while too many late payments are seen as a higher risk.

- Debt total amount: Any large debt amounts are considered higher risk, be it mortgage, auto loan, student loan, personal loan, or credit card debt.

- Length of credit history: The longer your history of accounts in good standing, the better your credit score.

- New credit accounts: Having too many new accounts may be seen as a sign of credit risk.

- Different types of credit: Having different accounts, such as a credit card and a loan, is known as having a “credit mix” and tends to help your credit score.

- Credit utilization ratio: Using more than 30% of your available credit lines makes you seem unreliable. As a result, any utilization that exceeds 30% will hurt your credit score.

What Constitutes a Good Credit Score?

The most common credit score ranges from 300 to 850 points. VantageScores considers 660-700 a good score, while FICO’s falls between 670 and 739. Scores above 800 are “excellent” or “exceptional” in both models – the highest tier possible.

A higher credit score increases your chances of loan approval. This “creditworthiness” helps determine how much you can borrow when applying for a mortgage and other types of financing, like car loans, personal loans. Credit scores also affect the credit limit on credit cards.

If your credit score indicates you’re well equipped to repay, lenders may offer you a lower interest rate, and you’ll pay less for borrowing. Unfortunately, the opposite is also true.

What Can Lower Your Credit Score?

Credit scores decrease through a combination of a person’s own actions, external factors like identity theft and fraud, or any combination of these.

These are the most common factors that impact your credit score:

Bankruptcy

A healthy credit score can go down hundreds of points after filing for bankruptcy, and the bankruptcy note stays on the report for up to 10 years.

Foreclosure

If you are delinquent on your mortgage payments, the lender can foreclose the mortgage by taking ownership of the property. Therefore, this negative mark bears a lot of weight and stays on the report for 7 years.

High credit utilization

Having one or more credit cards in good standing can help your credit score, but if you’re using more than 30% of your revolving lines of credit, it will depress your score. A smart move is to roll over balances between cards to get the overall utilization below the 30% threshold.

Late payments

Late payments tell lenders that you pose a risk they may not be comfortable with. Just one late payment can remain on your credit report for seven years.

Credit inquiries

Lenders look at your credit score with what’s called a credit inquiry, credit check or credit pull. There are two types:

| Hard inquiry | Soft inquiry |

| Tied to a formal loan or credit application | No formal loan or credit application linked to the inquiry |

| Lenders use it to accept or reject your application | Lenders and credit card issuers employ it to pre-approve candidates |

| Must be authorized | Prospective employers and even phone companies do soft checks as part of your evaluation |

| Remain on your report for up to two years | Looking at your own credit report counts as a soft inquiry |

| Too many can lower your overall score | Are only visible to you and don’t impact your score |

If any of these items are mistakes - for example, an unauthorized hard inquiry -, it’s up to you to request their removal. To remove negative items from your credit report, you can dispute the items yourself or employ the services of credit repair companies.

For personalized advice to improve your overall financial situation, look to credit counseling. Non-profit organizations such as the National Foundation for Credit Counseling (NFCC) can help you better understand your credit and improve your score over time.

Summary of Money’s Guide to Credit Scores

A credit score measures your creditworthiness and guides the creditor’s lending decisions on loan rates, terms, and loan amounts. Credit scoring companies use data from your credit report — a detailed record of your borrowing history and behaviors — to calculate your credit score. A healthy credit score is founded on good borrowing practices: on-time payments, moderate debt amount, and low credit utilization.

You need a good credit score to qualify for better loan terms and interest rates. A poor credit score does not prohibit you from borrowing money, but it’s a big obstacle for mortgage or car loan applications. Low credit limits your lender options, raises your interest rates, and can even disqualify your loan application.

More on Credit & Credit Repair

Money’s Top Selection Guides for Improving Your Credit

Money’s Credit Repair Companies Reviews |